High yield: a safe harbour in a brewing inflation storm?

Everyone in bonds fears inflation. Regardless of whether prices rise owing to monetary expansion or not, or whether inflation even occurs or not, the fear can cause volatility.

But given how low duration tends to be within high yield (around four years), then perhaps in these ‘junk’ bonds we have only fear itself to fear?

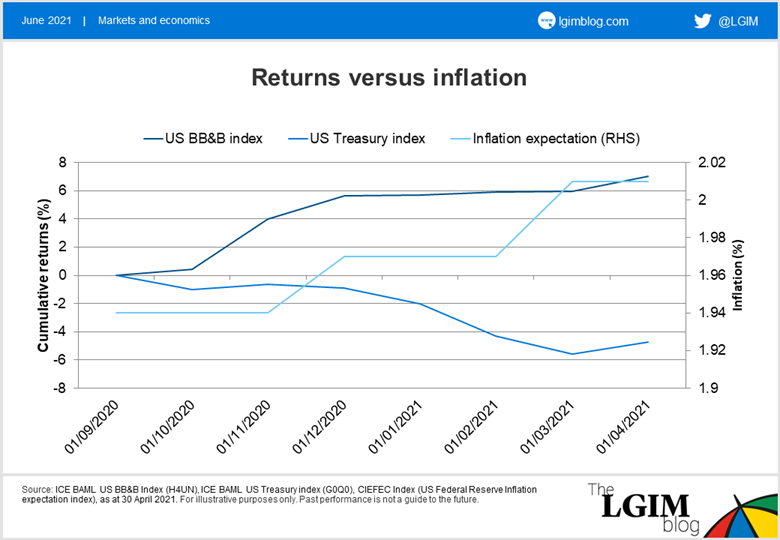

High yield, as it sits in fixed income, could wrongly be bucketed with its broader asset-class peers as highly correlated to rates and inflation risk. As the chart below shows, high yield has in fact had a much lower correlation to these factors, due to its lower duration and higher income. This combination can be a preferred mix for providing resilience in an inflationary environment.

We therefore believe investors should be able to find relative sanctuary within high yield as the inflation storm begins to brew. Over six months or so, we would expect that the income available from this asset class should act as a cushion against – and could potentially offset – yield increases due to normal interest-rate rises.

This could well restrict absolute returns, but may offer positive returns and relative outperformance versus investment-grade peers in an inflation-driven rates selloff.

Appendix: performance of indices cited

| ICE BAML US BB&B Index | ICE BAML US Treasury Index | |

|---|---|---|

| % | % | |

| 31.03.2016-31.03.2017 | 14.247 | -1.467 |

| 31.03.2017-31.03.2018 | 3.31 | 0.511 |

| 31.03.2018-31.03.2019 | 6.4 | 4.254 |

| 31.03.2019-31.03.2020 | -6.397 | 13.92 |

| 31.03.2020-31.03.2021 | 21.226 | -5.113 |

Related articles