Options for equity and derivative strategy

How can schemes seek to mitigate downside risk in 2024, while still targeting potential equity market upside if the Federal Reserve achieves a ‘soft landing’ in the US economy?

The following is an extract from our 2024 Solutions outlook.

In 2022 and 2023, equity returns were particularly choppy. As is typical, 2024 presents an uncertain environment where a plausible case could be made for multiple different trajectories for equities.

Whether the US Federal Reserve (Fed) has reached the end of its rate-hiking cycle and can engineer a soft landing in the US economy is particularly in focus. Let’s consider the potential implications of this scenario for equity markets.

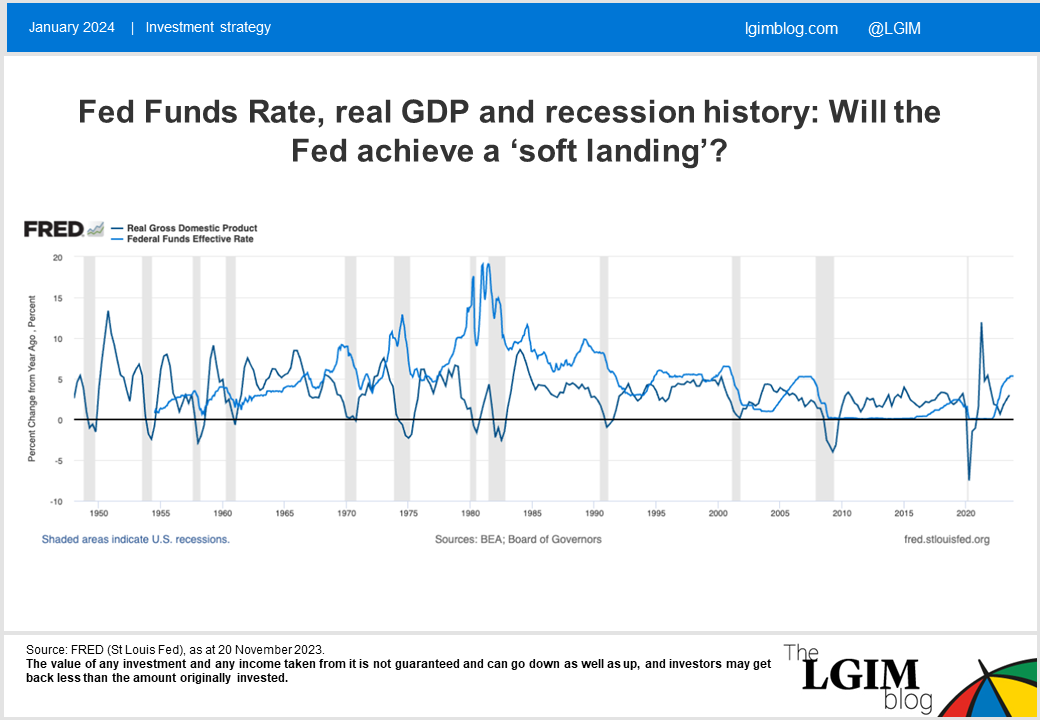

First, let’s look at historic soft landings after Fed hiking cycles. The FRED chart shows recessions (grey bars) and the Fed Funds Effective Rate back to 1950. Soft landings have not been all that common, but we can see that the mid-60s, mid-80s and mid-90s were all candidates for where recession did not follow a peak in the Fed Funds rate.

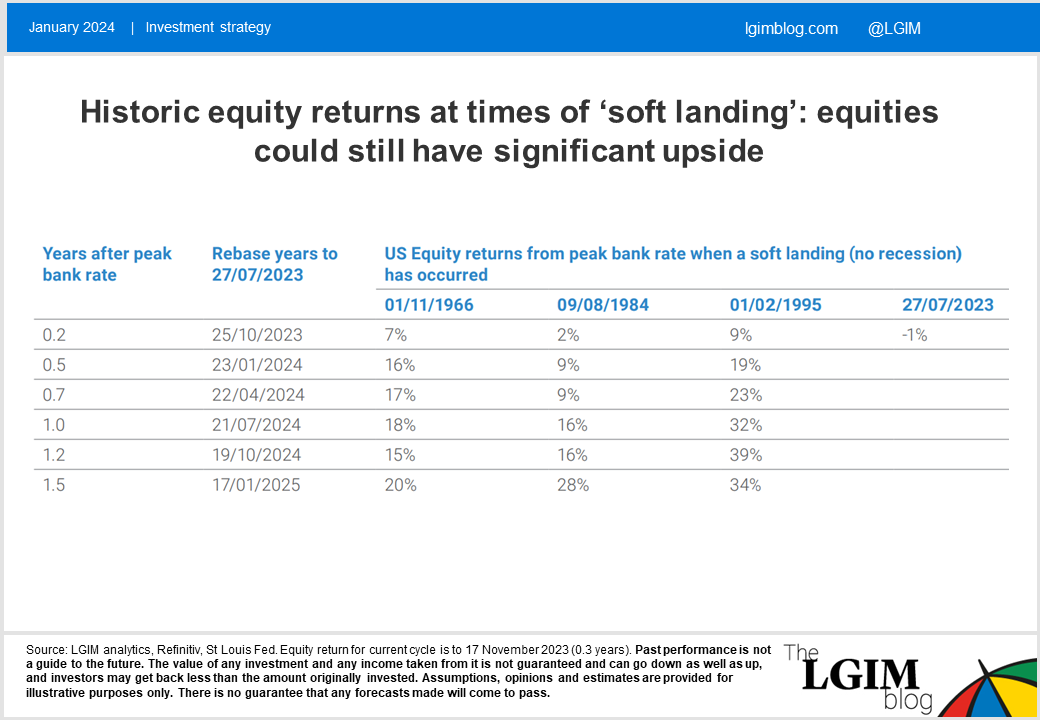

In these circumstances, we have recorded the S&P equity price return from the date of the peak Fed Funds rate for a period of 18 months. If the rate peaked most recently on 27 July 2023, that means 18 months from that point in the current cycle would take us to January 2025.

On that basis we note that, historically, if there has been no recession, the US equity market has been able to deliver very high returns (i.e. 20%+) over the 18 months after the peak in Fed Funds rate was reached.

This is not a prediction for 2024 equity returns but it is an observation that there could still be sizeable upside available in 2024 if things fall into place. As well as the Fed playing its role, the upside case for equities could also rely on improvements in technology, productivity increases and the ‘magnificent seven stocks’[1] playing a part given their heavy weighting in the index.

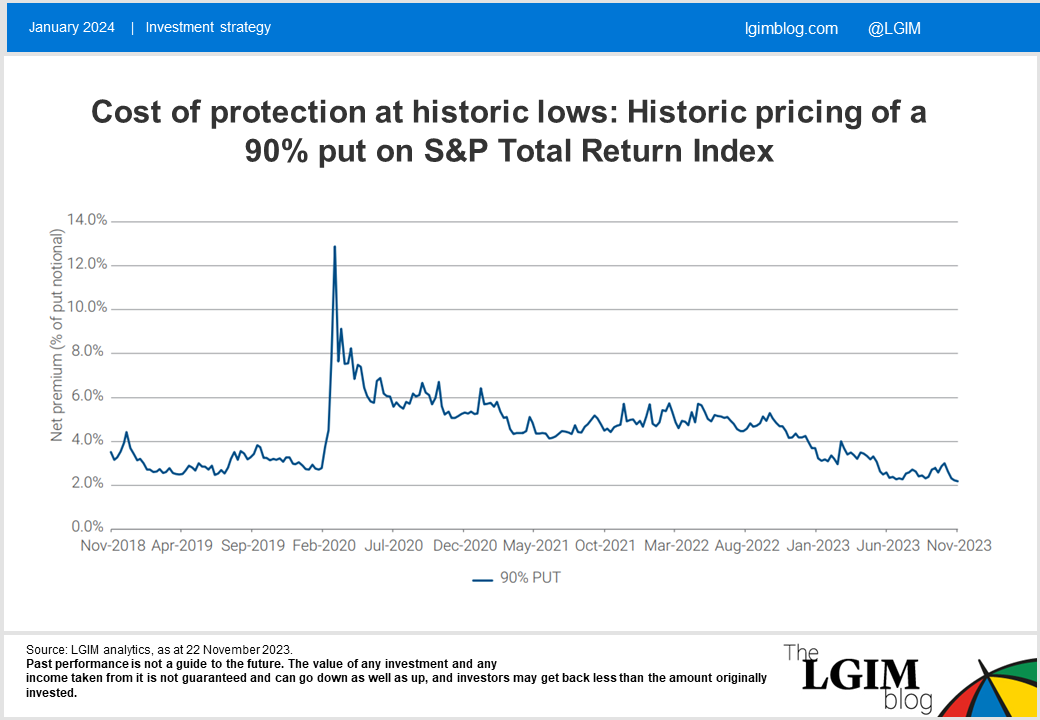

Next, we can see that part of the soft-landing narrative is visible in equity option markets, where implied volatility is around the pre-covid lows at the time of writing.[2] Combined with the high interest rate environment, this means that equity protection pricing is at the lows of the last five years as the chart shows.

The cost of equity protection (put options) could potentially be reduced further by either selling away upside or considering a put spread, however, we do not believe that current pricing offers compelling value given the potential for equity growth and the low level of implied volatility.

Although it’s important to be clear that while we do not have a central view that equity returns are likely to fall substantially in 2024, the headwinds are clearly there for all to see. In addition to changes in monetary policy, the following could potentially be troubling for equity markets:

- Geopolitical risk – if geopolitics come to the fore again the potential negative impact from disrupted supply chains and energy shocks could be problematic

- Political risk – in addition to the US election, Barclays note that 45% of the world population has an election in 2024

In summary, for an equity investor we observe that:

- The potential bullish case for equities is still on the table

- However, there are also notable downside risks

- Investors can seek to mitigate downside risk by paying a premium of around 2%

In our view, this approach offers pension schemes a potentially attractive way of preparing for more uncertainty in 2024, while taking advantage of the current low levels of option pricing and retaining notable upside exposure in the event that equity markets rise significantly

The above is an extract from our 2024 Solutions outlook.

[1] For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

[2] Source: LGIM analytics; 22 November 2023 versus 12 February 2020. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Florent Herelle

Head of Derivative Overlays

Florent is responsible for the design and management of derivative solutions with a particular focus on synthetic equity and segregated currency overlay strategies. Florent joined LGIM in 2009 as a fund manager within the Index Funds team before joining the LDI team in April 2013. Prior to that, Florent worked at KdK Asset Management in a fund structuring role and at Société Générale Asset Management Alternative Investments (in Paris) managing a range of derivative-based funds. Florent graduated from the University of Bordeaux (France) with masters’ degrees in Capital Markets and International Finance.

Celia Shen

Solutions Strategy Associate, Solutions Group

Celia is a member of the Solutions Group at LGIM. Celia joined LGIM in 2021 from Lane Clark and Peacock where she held the title of Investment Associate Consultant. Here she advised a range of institutional investors on their investment strategies. Celia graduated from the University of Oxford and holds a MMath in mathematics and statistics.

Related articles